Share this

Since landing in my new role at XYPN, I’ve been having a ton of great conversations. A few questions and comments have been a bit, well, perplexing. These center around the investment question and the infamous assets under management or AUM. Mostly because that’s what my new role entails, but also because that’s still what many associate with “financial ___________”. (I’ll leave it to you to fill in the blank; call it what you wish.)

For those I haven’t met yet, “Hello, I’m Brandon”, and I’m the Director of XY Investment Solutions (XYIS), XY Planning Network’s digital hybrid investment platform. It’s a turnkey asset management platform (TAMP) designed and curated to the specific needs of XYPN members (sales pitch over, kind of). With full disclosure of my role at XYIS, let’s dive into the questions.

Here is the paraphrased version of what people have been saying/asking:

Advisors Outside of XYPN:

“I didn’t think XYPN members managed assets. I thought they’re just a bunch of altruistic kids trying to save the world with financial planning.” #winning

XYPN Members:

“I’m not sure about managing assets. I like to keep things clean, pure and free of all conflicts. I’m not even sure you can do AUM and be fee-only.” #fail

Random Consumers (Your Potential Clients):

“Wait! So you’re telling me there are advisors out there who will map out my financial life, organize and manage my jumbled accounts which total not enough and I can pay them like my monthly Orangetheory bill?” #opportunity

Ok....what’s the point of all this? The point is there is literally no one on the planet better positioned to manage assets in the right way, with an amazing experience, for a very reasonable cost than fee-only advisors. I mean...check out the recent Jason Zweig article in the Wall Street Journal titled , “The 19 Questions to Ask Your Financial Advisor”. We can literally check ALL OF THE BOXES!

So, what exactly is happening in our profession? And is your firm positioned to take advantage of the coming wave? Let’s paraphrase how the industry headlines are being perceived by the various segments.

Traditional brokers + the wirehouse crowd (yes they still exist and unfortunately people still use them.)

“We don’t read headlines...we are the headlines”...Thank you Bobby Axlerod, that attitude seems about right. Next!

Broker-dealer types and wirehouse people trying to do the right thing but can’t

“The robots are coming, the robots are coming….and they’re coming on a white fiduciary horse and they’re bringing fee compression hell with them and there’s nothing we can do about it!!!!”

Traditional RIAs

“The robots are coming, the robots are coming…and they’re bringing fee compression hell with them!”

XYPN Members

“Let’s program the robots to do all the #@$%@$ work so we can create a rich life for our clients and ourselves!”

Mic drop? Not quite, but it’s a nice head start. And this is where those questions about managing assets come back into play. What is the one element that is just CRUSHING to each of the firms above with the one singular exception being XYPN advisors?

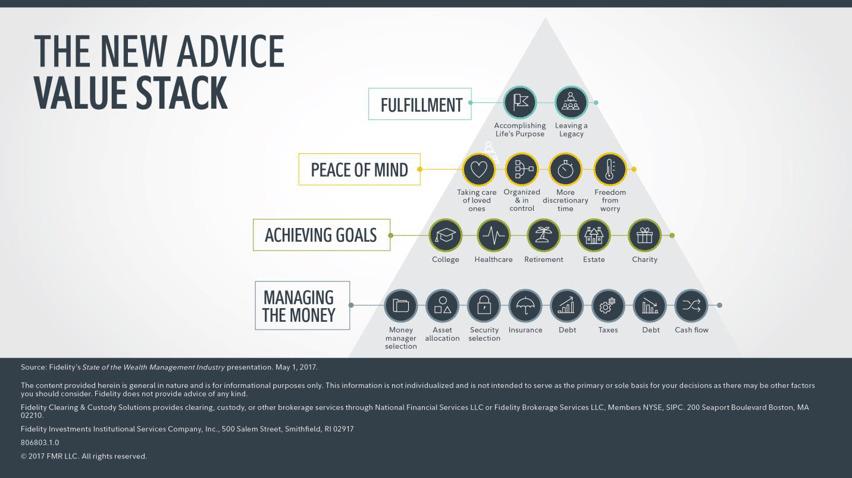

They are all a slave to AUM. For the last 30 years, they haven’t been “advisors” or “wealth managers” or even “planners”, they’ve been asset gatherers wandering through concrete jungles rummaging for the next % squeeze of bps. They centered their value on the bottom of the value stack and they’re now trying to flip the script but can’t.

The XYPN AUM Advantage

XYPN members lead with planning. Always have. Always will. Their clients pay them for that and that is where they see the value. That is absolutely not the case for most advisors. Ask any client what they pay their “advisor” for and the answer in almost all cases is, “I pay them to manage my money”.

For XYPN members, their value to clients is all at the top of the pyramid, and that’s what their clients pay them to do. Their value isn’t even in the plan itself, the value is in the...wait for it...cliche answer coming up…the value is in the process! It’s in the judgement and discipline they apply to the ongoing tweaks, course corrections and trade-offs that happen on a daily basis!

So where does AUM play into all of this? Well, I’m glad you asked and I think we are going to have a great relationship because that’s what I was going to talk about next.

Each of your clients has money in some form or fashion. Whether a little or a lot, it all matters to them and they want and need help with it. And regardless of what we may feel about our place in this world, financial planning isn’t mainstream. Most clients are not coming to you because they have a “financial planning” problem, they are coming because they have a “money” problem. That decision point to seek help usually starts with money (i.e., I need someone to help with my 401k) and they then stumble upon something better! I know. It’s sad and I wish that wasn’t the case but let’s just pretend we are EDM about to go mainstream.

Why AUM?

There are a multitude of reasons why it makes sense to add an AUM solution to your offering to clients and we will highlight those in a second. But let us start with the most basic, honest and heartfelt answer we could come up with:

Because you can help.

Your clients trust you can do it and do it right. People want help and you can give it to them. It IS that simple. Don’t complicate it any more than that.

Oh…..but let’s complicate it. We are human after all and if I’ve learned anything in my short time here, “because we can” isn’t going to fly. So once again, thanks for the segue.

Our Behavior Sucks

That’s right. We ARE human. And as humans we are subject to what? Behavior! Cue Kahnemann, Thaler, someone throw up a Carl Richards sketch! This isn’t about “managing money”, it’s about managing behavior. You need two keys for the nuclear codes because, left to their own devices, clients will inevitably flip the red switch and turn the key. They need you to talk them off the ledge and you can’t do that if you’ve passed them off to the latest robo advisor or fund company giant.

Your rebuttal: “I don’t have to be managing their assets, they text me and I advise them not to do that.” Let’s see how that works out when the market tanks by 20%, the fake news is piling on and they’re literally one “swipe right” from cashing it in. Remember, it’s not always about what we help our clients do. It’s also about what we help them NOT do.

The Client Experience Matters

In a world where your last great experience is your new level of expectation, you have to be able to deliver and deliver in a big way. Clients are coming to you because they have a problem they want you to solve. Embrace that. You don't want to be like the LifeLock commercial and just “monitor” the situation; solve it for them. Then show them the true value of working with you. With the technology available today, you can solve the investment problem with an amazing experience (mobile, digital), that delivers sophisticated yet simple solutions and with little time or expertise on your end.

The Price is Right

Remember that addiction problem with AUM we talked about? You don’t have it. So when you go to price your services, you can price it according to the new paradigm and have it included in your service model as such - just piece of an overall puzzle. More on this in future posts, but know your niche and price accordingly. If your clients don’t shop at Wal-Mart, don’t price your services that way.

Plus, it’s not an all or nothing model. AUM works great when combined with other pricing models. Across the spectrum at XYPN, our members have have dozens, if not hundreds, of combinations of pricing structures all geared to fit the unique needs of their clients.

The World is Not Set-It-and-Forget-It Anymore

No, I don’t mean moving everything to a tactical, actively managed strategy. What I mean is that the rate of innovation and change on the product side of the investment world is almost as staggering as the tech world. Most of us at XYPN believe in a globally diversified passive strategy using the lowest cost vehicles possible. But which ones? And what happens when they change ala TD Ameritrade’s recent shift. The landscape is changing and changing fast and it’s not going to stop. If it was a set-it-and-forget-it world, your clients would still be good in their ‘C’ share mutual funds, right?

Authenticity always wins. Embrace the conflict

AUM can be a conflict of interest. Not always, but it can. There. We said it. BUT...members of XY Planning Network have all signed a Fiduciary Oath vowing to put clients’ best interests before their own and disclose any potential conflicts to them. So, as long as you’re trying to do what’s right and act in your fiduciary capacity, there’s nothing to worry about. Embrace it with yourself and with your clients.

It’s just good business.

If you can effectively and efficiently solve your client's needs in one place, in a fee-only manner with limited conflicts of interest, why wouldn’t you want to do that? It’s a great experience for them and it’s good business for you. #winwin

The Value of...YOU

This could be a whole post in and of itself, but value is always in the eye of the beholder. And if the “beholder” is your clients, what is the one question they all ask, no matter the circumstance, situation, time frame, age, whatever? The question every client asks is this:

Am I ok?

The value of every advisor is in answering that question.

Whether adding AUM to your repertoire makes sense for you, as long as you are constantly answering that question for your clients, you are going to be just fine.

Written by Brandon Moss, Director of XY Investment Solutions

For those I haven’t met yet, “Hello, I’m Brandon”, and I’m the Director of XY Investment Solutions (XYIS), XY Planning Network’s digital hybrid investment platform. It’s a turnkey asset management platform (TAMP) designed and curated to the specific needs of XYPN members (sales pitch over, kind of). Visit XY Investment Solutions

Share this

Subscribe by email

Getting Involved in the Financial Planning Community - What Would Arlene Say?

Mar 15, 2018

12 min read

An Advisor’s Best Friend: The Ability to Say “No”

May 12, 2016

4 min read