These Related Stories

Share this

While negative policy rates and negative yielding bonds are still somewhat of a recent phenomenon, the amount of negative yielding debt has been growing over the last few years, and the concept is rather counterintuitive (and not surprising, there are many different opinions on what comes next). In this blog, we dive into multiple aspects of this phenomenon to help start the conversation.

Let’s start with some numbers

According to Bloomberg, as of August 30, 2019 there was in excess of $17T in negative yielding debt globally, which they cite as 30% of all investment grade securities1.

How did we get here?

Negative rates really started with various non-US central banks as they attempted to jumpstart their flagging economies after the Great Recession. The idea went something like this: central banks would penalize banks for holding their deposits (i.e. setting negative policy rates); banks would lend out the money rather than be charged; the borrowers would spend the money; leading to economic growth and inflation. The reality, however, has been different as negative policy rates have not created the expected pickup in economic activity (could their economies be worse off without the negative rates?). In fact, no country that has set negative policy rates has moved away from them. One could suggest it is a growing issue as governments/lenders/consumers become accustomed to negative rates and the amount of negative yielding debt continues to grow, and now includes corporate debt as well as sovereign debt.

What are negative rates/yields?

Negative yields are exactly what they sound like. They are bonds that have negative, not positive, yields to maturity. For bonds issued with negative yields (yes, these actually exist today), the easiest example to demonstrate is an investor purchasing a bond with a guarantee to receive less than the invested amount at maturity (no, negative coupons are not collected). In short, when purchasing bonds with negative yields, you are effectively paying someone for lending them money! You can also have a negative yield to maturity even if the coupon is positive by paying more for the bond than you will receive in return after adding up the remaining coupons and return of par value. As you can imagine, these are not concepts regularly taught in finance or economic textbooks.

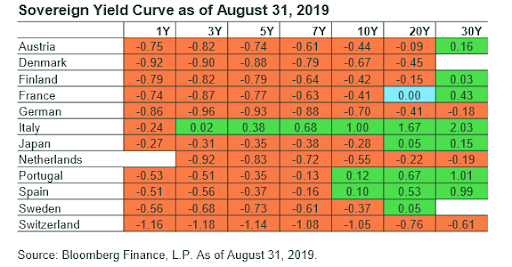

How pervasive are negative yields?

The chart below shows the various key rate durations across many non-US sovereign yield curves. The orange boxes highlight negative yields. For countries like Germany and Switzerland, the entire yield curve is negative.

How do negative yields impact the return of a bond?

Remember, there are two components to a bond’s return: 1) income and 2) capital appreciation. In its simplest form, the income return is the component generated from the stated interest rate. For example, a $100,000 bond with a 2% interest rate will generate $2,000 of income per year. The second component, capital appreciation, occurs when the bond is worth (or sold for) more than you paid for it. In this instance, if you buy a Treasury bond today, it could be worth more in 6 months if there is a flight to safety. With negative interest rates, the two components are the same, but different. In Germany, investors are in essence paying the government for the privilege of lending them money (i.e. negative income). However, prices still move inversely with yield so as long as yields continue to fall, there is still the potential for price appreciation. In other words, in order to expect a positive return on the bond, the capital appreciation of the bond must outweigh any impact from the negative yield.

For international bonds, a separate component of return (and volatility) comes from the impact of currency. As the volatility impact from currency can often be quite large, we would generally recommend hedging non-US fixed income investments. Interestingly, given the current environment where US rates are so much higher than non-US rates, US investors can also earn return from their hedging activities.

As an example, the reported yields of various Bloomberg Barclays indexes are as follows as of 8/31/192:

US Aggregate: 2.09%

Global Aggregate unhedged: 0.36%

Global Aggregate hedged USD: 2.67%

Interestingly, while this situation can be a positive for US investors, it is the same rationale that can dissuade global investors from making sizable investments in US fixed income.

What are the implications for negative yields?

This is where the answer becomes more complicated; it depends on who you are. Banks, for example, are likely losers in a world of negative rates, though don’t be surprised as banks introduce new fees with the goal of recouping some of the loss from negative interest rates. Savers are also hurt by negative rates as they are not receiving any income on their fixed assets. However, it is possible for consumers to see pockets of benefit. For example, some countries have negative mortgage rates. In these instances, homeowners receive a credit to their monthly mortgage amount. Similarly, low/negative policy rates, and in turn bond yields, have driven money to ‘risk assets’ outside sovereign debt in the never-ending search for more yield.

Can rates in the US go negative?

Right now, there aren’t many economists or analysts predicting negative rates in the US. However, at the same time we also can’t say the scenario is outside the realm of possibility. If there were to be a US and/or global recession, this would likely make US government bonds even more attractive, which would then push up their prices and push down their yields. Let’s just say we aren’t convinced it can’t happen here.

How does this end?

No one can say for sure as this “experiment” is still relatively new to the world of global finance. One item that seems fairly clear, though, is that monetary policy is reaching its limits on what it can do. Central banks have been quite aggressive in keeping rates low (or negative) and yet it is widely believed the expected results have not materialized. Governments may be forced to consider more fiscal policy measures (e.g. taxes, spending) as a tool going forward.

About the Authors

Mario Nardone, CFA

Partner, East Bay Investment Solutions

Mario began his investment career in 1999 with Vanguard mutual funds in Valley Forge, PA, where he consulted institutions and financial advisors on investment policy, portfolio construction, and Exchange-Traded Funds (ETFs). He also held roles as a research analyst, a municipal bond fund specialist, among others during his tenure. In 2003 he earned the Chartered Financial Analyst designation, and he continues to mentor aspiring Charter candidates and young investment professionals.

Mario relocated to Charleston in 2010 to serve as Chief Investment Officer for a financial planning firm before establishing East Bay, the collaborative partner firm of (insert firm name), in 2014. As a Partner at East Bay, Mario serves a select group of Registered Investment Advisor firms as their outsourced Chief Investment Strategist. Responsibilities of this role include continuous oversight of advisor clients’ investments, bespoke strategies for unique situations, client communications, and more.

Mario is Past President of CFA Society South Carolina and Former Chairman of the College of Charleston Finance Department Advisory Board. His approach to investments and the industry has been featured in Investment News, NAPFA Advisor Magazine, South Carolina Public Radio, and other publications and media outlets.

Mario enjoys early morning basketball games, the Charleston beaches and restaurant scene, and spending summers in coastal Maine. He is an avid world traveler and SCUBA diver, but also enjoys the simpler joys of life with his wife Piper, their daughter Pepper, and son Santino.

Learn more and connect with Mario on LinkedIn

Eric Stein, CFA, joined East Bay Financial Services in 2018 and brings his passion for investing and client service with him. He enjoys sharing his knowledge and experiences with colleagues and clients.

Prior to joining East Bay, Eric has worked for a variety of firms both large and small. This includes 7+ years with Goldman Sachs Asset Management where he held roles in areas such as performance measurement, client service, risk analysis and portfolio construction. He also served as the Chief Investment Officer for RSM U.S. Wealth Management for 10+ years, providing strategic leadership and solutions for their national investment platform.

Eric is a proud graduate of Indiana University where he earned a B.S. in Finance. He also earned the Chartered Financial Analyst (CFA) designation in 2001 and continues to stay involved in the local society.

Sources

- https://www.bloomberg.com/graphics/negative-yield-bonds

- PIMCO, Bloomberg - Note: US Aggregate Index refers to the Bloomberg Barclays U.S. Aggregate Index

Disclosures

The commentary contained herein is intended to be general and educational in nature, and is not intended to be used as the primary basis for investment decisions, nor should it be construed as advice designed to meet the particular needs of an individual investor. Nothing contained herein should be considered legal, tax, accounting, investment, financial, or other professional advice, and should not be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation of any security or other financial product or investment strategy. Investors should consult with a qualified professional advisor before taking any action based on this commentary.

Investing in mutual funds, exchange-traded funds (“ETFs”), and other equity and debt securities involve risks, including loss of principal. Any performance data quoted represents past performance. Past performance does not guarantee future results and principal value will fluctuate so that an investor’s investments, when redeemed, may be worth more or less than their original cost. Performance data quoted does not account for any advisory fees imposed by XYIS or any independent and unaffiliated financial planners, or other transaction charges, expenses, taxes, or other fees and costs. Performance of an investor’s actual portfolio will differ from any performance presented.

Investing in foreign securities may involve certain additional risk, including exchange rate fluctuations, less liquidity, greater volatility and less regulation. Small company stocks may be subject to a higher degree of market risk than the securities of more established companies because they tend to be more volatile and less liquid. Bonds are subject to risks, including interest rate risk which can decrease the value of a bond as interest rates rise. REIT investments are subject to changes in economic conditions and real estate values, and credit and interest rate risks.

Investors cannot invest directly in an index. Indexes are unmanaged and reflect reinvested dividends and/or distributions, but do not reflect sales charges, commissions, expenses or taxes.

An investor should consider a portfolio’s investment objectives, risks, charges and expenses carefully before investing. The underlying funds’ prospectus contain this and other important information. Please read any applicable prospectus carefully before investing.

About XY Investment Solutions, LLC

XY Investment Solutions, LLC (“XYIS”), through its partnership with East Bay Financial Services, LLC (“East Bay”), builds investment models through a technology solution, and supports financial planners with investment strategies based on research, experience, and sound rationale. XYIS primarily allocates client assets among various mutual funds and/or ETFs. XYIS may also allocate client assets in individual debt and equity securities, options and independent investment managers. XYIS's services are based on long-term investment strategies incorporating the principles of Modern Portfolio Theory. XYIS manages client investments in portfolios on a discretionary basis. Visit xyinvestmentsolutions.com to learn more.

Share this

Subscribe by email

Reaching for Yield: A Careful Analysis

-1.png?width=360&height=188&name=Reaching%20for%20Yield%20A%20Careful%20Analysis%20(1)-1.png)

Reaching for Yield: A Careful Analysis

Sep 5, 2022

8 min read

ESG Investing

ESG Investing

Jul 9, 2018

4 min read

A $1-Trillion Shift and What You Should Know